ESG in commercial real estate used to be a story about ambition: net-zero pledges, green certificates, bigger reporting frameworks. In 2026 the story is quieter and harder. The frameworks are being trimmed, not expanded. Assurance is arriving. And the question every regulator, investor, and auditor now asks is the same one: can you prove the number?

That shifts the ground under every sustainability team. The bottleneck is no longer writing the report. It is getting utility data that is complete, accurate, and traceable enough to survive an audit. Every trend below leads back to that single point.

Here are the five ESG trends shaping commercial real estate in 2026, and what each one means for the data underneath your reporting.

1. The rules got simpler, but the data bar got higher

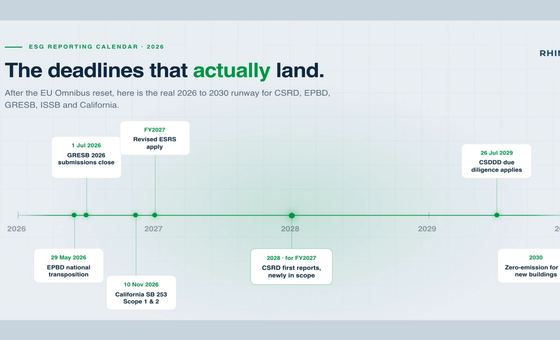

The biggest ESG story of the past year is the EU's Omnibus package. Adopted by the Council in February 2026, it sharply narrows who has to report under the Corporate Sustainability Reporting Directive (CSRD): the threshold moves to companies with more than 1,000 employees and over €450 million in turnover, and the ESRS reporting standards are being cut back to prioritize core quantitative data. Thousands of firms that were bracing for full CSRD reporting are now out of scope or on a lighter track.

It would be easy to read that as pressure coming off. It isn't, for two reasons.

First, the regulations that bite real estate hardest are not CSRD. The recast Energy Performance of Buildings Directive (EPBD) sets a hard trajectory: worst-performing non-residential buildings must improve to energy class E by 2030 and D by 2033, with a zero-emission stock by 2050. The EU Taxonomy still screens assets against energy-performance thresholds. In the UK, commercial MEES is pushing let property toward EPC B by 2031. City-level building performance standards, from New York's Local Law 97 to European energy-label mandates, carry fines regardless of what CSRD asks. None of these were simplified. All of them are measured at the building, on actual energy performance.

Second, for the companies still in CSRD scope, the ESRS still demand real energy and emissions data, and that data now needs limited assurance. When an auditor signs off, every figure has to trace back to a source, with a documented method for how it was collected and attributed. A cleaner report is not an easier report. It is a report where the numbers are checked.

There is also a party the Omnibus never touched: investors. Lenders, funds, and GRESB participants still expect the same energy and emissions data they asked for last year, whether or not a company files under CSRD. Lighter regulation has not meant lighter expectations, a mismatch worth reading in full in The Omnibus Paradox: less regulation, same investor expectations.

What it means for your data: fewer pages, higher standard of proof. The reporting you keep has to be built on utility data you can stand behind, line by line.

2. "Estimated" is quietly being pushed out

For years, portfolio ESG reporting ran on estimates. Missing a tenant's electricity data? Extrapolate from floor area. No submeter on the heating? Model it from a benchmark. It got a number into the report, and for a long time that was enough.

That tolerance is closing. GRESB, the benchmark most institutional real estate investors watch, tightened its data estimation rules for the 2026 assessment: estimated data may not exceed 20% of the period for which actual data exists, and every estimate has to be built from actual metered data specific to that asset. Verified data scores higher. The direction is unambiguous, actual meter readings are the baseline, and estimation is the exception you have to justify.

Assurance pushes the same way. Under limited assurance, an estimate with no metered basis is exactly the kind of figure that gets flagged. The quality hierarchy is now explicit: measured beats modeled, and metered beats benchmarked.

This is the shift that matters most, because it changes what "good" looks like. ESG reporting is moving from estimation to measurement, and the buildings that win are the ones with the most complete metered coverage.

What it means for your data: the gaps you used to fill with assumptions are now the gaps auditors and benchmarks penalize. Closing them means metering coverage across the portfolio, not just the head-lease meters.

3. Scope 3 and the tenant data problem

Ask any sustainability lead in real estate what keeps their reporting incomplete, and the answer is almost always the same: tenant data. In a multi-let building, the energy a tenant uses inside their own space is often the landlord's Scope 3 emissions, and it is frequently the single largest slice of the building's footprint. It is also the hardest to see.

The reason is structural. Tenant spaces are often not submetered, so the landlord has no direct reading of what happens behind the tenant's door. Utility bills sit with the occupier. The classic split incentive applies, the landlord would invest in efficiency, but the tenant pays the energy bill, so neither side moves. The result is a portfolio-wide blind spot exactly where the emissions are largest.

The best-practice answer is not a better estimate. It is submetering. Metering tenant spaces turns Scope 3 from a modeled guess into a measured figure, and it removes the annual scramble to chase occupiers for utility bills that may never arrive. Where submeters genuinely are not feasible, floor-area apportionment remains a fallback, but it is now clearly the lower-quality path, and benchmarks and auditors treat it that way.

What it means for your data: the tenant layer is where reporting quality is won or lost. Submeter-level data is what lets you report Scope 3 on actuals instead of assumptions, and it makes transparent tenant billing possible at the same time.

4. AI moved the bottleneck, it didn't remove it

Every ESG software vendor now has an AI story: automated report drafting, framework mapping, anomaly detection, benchmarking against GRESB or ENERGY STAR. Much of it is genuinely useful. Automation can compress a reporting cycle that used to take weeks into days, and pattern-detection can surface energy waste a human would miss.

But AI has not changed the fundamental constraint. It has moved it. When drafting and calculation are automated, the limiting factor becomes the quality of the data going in. ESG data is notoriously heterogeneous, fragmented across systems, incomplete, and inconsistently formatted, and no model fixes a number that was never measured. Point an AI reporting engine at a portfolio that is half estimates and manual spreadsheet reads, and it will produce polished, confident, wrong reports faster than ever.

The practical consequence is that the smart investment in 2026 is upstream, not downstream. Automated, verifiable data collection is what makes everything above it work: the AI analysis, the framework mapping, the assurance sign-off. The audit trail matters as much as the number, source system, timestamp, and method attached to every data point, because that is what an assurance provider asks to see.

What it means for your data: buy the reporting layer you like, but only after the collection layer is solid. Clean, sourced, automated utility data is what turns AI from a liability into a genuine time-saver.

5. The same data pays for itself in operations

Here is the part that gets lost when ESG is framed purely as compliance. The utility data you collect to satisfy a regulator is the same data that cuts your operating costs, and in 2026 more owners are treating it that way.

Interval-level consumption data does two jobs at once. For the report, it gives you measured, auditable numbers. For the building, it shows exactly where energy is going: the meter running overnight for three weeks, the HVAC schedule that never switches off, the one asset in the portfolio dragging the average down. That visibility is what makes decarbonization and retrofit decisions concrete instead of theoretical, and it is where the cost savings live.

This is why the framing of "ESG data" as a reporting overhead is increasingly wrong. Granular metered data is an operational asset. It funds the electrification business case, targets the retrofit spend, and catches the billing errors that quietly eat margin, all from the same feed that populates the ESG report. What gets measured gets managed, and in commercial real estate the measuring finally pays for itself.

What it means for your data: collect it once, use it twice. The metering that makes your reporting audit-ready is the same metering that makes your buildings cheaper to run.

The through-line: better data, not more reporting

Read the five trends together and the pattern is clear. Regulation is consolidating around fewer, higher-quality disclosures. Estimation is giving way to measurement. Scope 3 depends on seeing tenant consumption. AI is only as good as its inputs. And the same data drives both compliance and cost. Every one of them rewards the same thing: complete, accurate, traceable utility data across the whole portfolio.

That is the hard part, and it always has been. Not the report, the data underneath it. Utility data in commercial real estate is spread across smart meters, submeters, building systems, and utility providers, in different formats, often still landing in spreadsheets at quarter-end. Pulling it together, verifying it, and keeping it audit-ready is where sustainability teams lose weeks and where reports go wrong.

This is exactly what Rhino does. Rhino collects and automates utility data, electricity, gas, water, and heat, including submeters, across your portfolio. It connects through smart-meter connections or Rhino's own hardware, works with your existing building infrastructure without an overhaul, and delivers data that is ready to feed CSRD, GRESB, and EPBD reporting without the manual scramble. Complete coverage, actual meter readings, and a clear trail back to source, which is precisely what 2026's trends demand.

The ESG conversation in real estate has grown up. It is no longer about who has the boldest pledge. It is about who can prove their numbers. That starts, and ends, with the data.

FAQ

What are the biggest ESG trends in real estate for 2026?

Five stand out: the EU Omnibus package narrowing CSRD scope while assurance raises the proof bar; benchmarks like GRESB pushing from estimated data to actual meter readings; Scope 3 tenant data becoming the main reporting gap; AI shifting the bottleneck to data quality rather than removing it; and utility data increasingly used for cost savings, not just compliance. All five reward the same thing: complete, accurate, traceable utility data.

Does the CSRD Omnibus mean real estate companies can stop worrying about ESG data?

No. The Omnibus, adopted in February 2026, raises the CSRD reporting threshold to companies with more than 1,000 employees and over €450 million in turnover, and simplifies the ESRS standards. But the regulations that hit buildings hardest, the EPBD recast, the EU Taxonomy, UK MEES, and city building-performance standards, were not simplified. They are measured on actual building energy performance, so accurate utility data still matters regardless of CSRD scope.

Why is estimated ESG data becoming a problem?

Because assurance and benchmarks now favor measured data. GRESB's 2026 assessment caps estimated data at 20% of the period with actual data and requires estimates to be based on real metered readings. Under limited assurance, figures without a metered source are the ones auditors flag. The reporting standard is shifting from estimation to measurement.

How do landlords collect Scope 3 tenant energy data?

The reliable method is submetering tenant spaces, which turns Scope 3 emissions from a floor-area estimate into a measured figure and removes the need to chase tenants for utility bills. Where submeters are not feasible, apportioning by floor area is a fallback, but it is treated as lower-quality data by both benchmarks and auditors.

Can AI solve ESG reporting for real estate?

AI can automate drafting, framework mapping, and anomaly detection, and it can compress reporting cycles significantly. But it cannot fix data that was never measured. The constraint has moved upstream to data quality, so the priority in 2026 is automated, verifiable data collection with a full audit trail, source, timestamp, and method, before adding an AI reporting layer on top.

How does Rhino help with ESG data collection?

Rhino collects and automates utility data, electricity, gas, water, and heat, including submeters, across a commercial real estate portfolio. It connects via smart-meter connections or its own hardware, works with existing building infrastructure without an overhaul, and delivers audit-ready data that feeds CSRD, GRESB, and EPBD reporting without manual collection.