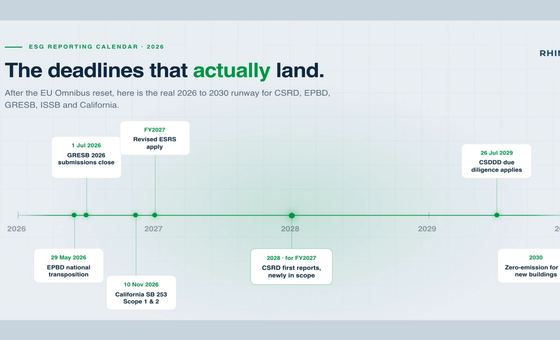

Governments worldwide are rapidly tightening ESG disclosure rules. In Europe, the Corporate Sustainability Reporting Directive (CSRD) will compel most large companies (including property firms) to publish detailed annual sustainability reports in 2025–2026. The CSRD significantly broadens the old Non-Financial Reporting Directive (NFRD): for example, its first wave requires large listed companies to report FY 2024 data in 2025. CSRD reports must follow the European Sustainability Reporting Standards (ESRS) set by EFRAG. Crucially, the CSRD/ESRS regime uses a double-materiality approach: firms must report both on how ESG factors affect their business and how their operations impact people and the planet. In short, real estate companies will need to identify all material sustainability impacts, risks, and opportunities in their value chain (energy use, emissions, climate risks, labor issues, etc.) and disclose them in a standardized format. This alignment with the EU Green Deal’s goals means the CSRD (together with the EU Taxonomy and related laws) is meant to direct capital toward sustainable activities and improve ESG transparency.

Key EU Deadlines and Scope

CSRD reporting is being phased in by company type. The broad schedule is:

FY2024 (reports in 2025): Large listed companies (excluding micro-entities) on EU markets. This includes most publicly traded REITs or listed property developers.

FY2025 (reports in 2026): All other EU-based large companies (≥250 employees AND ≥€50 million turnover or €25 million assets) and parent companies of groups meeting that threshold. Many big property owners and RE funds will fall here.

FY2026 (reports in 2027): EU-listed small/medium enterprises (SMEs), plus certain financial institutions (like smaller banks and insurers).

FY2028 (reports in 2029): Non-EU companies with significant EU activity. This includes any parent company (even outside the EU) that generates >€150 million in EU turnover and has an EU subsidiary or branch meeting the size tests.

During their first CSRD year, companies must obtain independent limited assurance on their sustainability report; reasonable assurance is expected to follow later. Note that EU “omnibus” and “stop-the-clock” legislation have slightly adjusted these dates for some firms, but the above is the working timeline. In practice, compliance should begin immediately: companies typically use the prior year’s data and need time to build processes for CSRD disclosures. U.S. firms with EU operations are also caught – about half of the 50,000 new companies in CSRD’s scope are non-EU entities, and they too must follow ESRS when reporting on their EU businesses.

Other Global Frameworks

Beyond CSRD, property firms should track several other standards and taxonomies:

EU Taxonomy. This is a classification system for “sustainable” economic activities. It sets technical criteria (e.g., energy efficiency thresholds for buildings) to define whether an activity substantially contributes to climate goals without harming other objectives. Real-estate owners must disclose, for their portfolios, the share of assets (by floor area, turnover, or investment) that meet the Taxonomy’s standards. The Taxonomy “provides a framework to align real estate investments with sustainability goals, promoting environmental and social responsibility” in the sector. Aligning with it offers a clearer path to meet investor and regulator expectations. In practice, this means gathering building data (e.g., energy performance certificates and renovation plans) to calculate Taxonomy alignment.

TCFD / ISSB (IFRS S1/S2). Globally, the Task Force on Climate-related Disclosures (TCFD) has long influenced climate reporting. Its principles (governance, strategy, risk management, metrics) have been codified into new ISSB standards: IFRS S1 (general sustainability disclosures) and IFRS S2 (climate-specific disclosures). Both S1 and S2 take effect for annual reports starting Jan 1, 2024. While not EU law, many investors and multinationals will follow IFRS S1/S2 (which are explicitly based on the TCFD recommendations). In short, these standards mean even outside Europe, large real-estate firms will soon face rigorous climate-risk reporting requirements.

Other countries rules. In the U.S., the federal SEC’s climate rule has stalled, but states are acting. California’s SB 253/261 will require large companies (>$1 billion revenue) to report Scope 1 & 2 emissions starting in 2026, then Scope 3 in 2027, plus a climate-risk report by Jan 2026. New York, Illinois, and others may follow suit. Overall, about half of the companies that the SEC would have covered now need to comply with state or foreign rules instead.

A key point is consistency: any climate disclosures should align broadly with TCFD/IFRS templates (governance, targets, scenario analysis, GHG inventories, etc.). In practice, real-estate firms will likely produce one core ESG report per year covering all frameworks (CSRD/ESRS in Europe, IRSB elsewhere) and then map the data to each standard.

What Data to Gather

Under these rules, property owners must compile a wide range of sustainability data. Key categories include:

Energy consumption and efficiency. Metered energy use (electricity, gas, district heating, etc.) for each building is fundamental. Many EU countries also require Energy Performance Certificates (EPCs) for buildings; those ratings and the underlying energy consumption are now crucial inputs to both CSRD/ESRS and the Taxonomy. In practice, firms should automate meter reading and billing data (via building management systems or utility dashboards) to avoid errors. Platforms exist to centralize this – for example, one real-estate energy system “directly integrates with meters for reliable provision of your energy data in real time / 15-minute intervals” and stores it centrally. Such continuous data makes it possible to benchmark and report on energy intensity and efficiency trends.

Greenhouse gas emissions (Scopes 1, 2, 3). Scope 1 (direct fuel combustion and on-site generation) and Scope 2 (purchased electricity) emissions are reported for owned properties. Importantly, CSRD explicitly requires Scope 3 reporting for value-chain emissions. For real estate, Scope 3 is usually dominated by tenant energy use (downstream leased assets) and embodied carbon (construction materials). If a landlord does not control tenant energy contracts, tenant usage falls under Scope 3. The GHG Protocol’s “downstream leased assets” category covers this. In fact, any company leasing buildings “will need to collect and report tenant energy data and be able to classify it as Scope 1, 2, or 3 depending on control”. In other words, even “indirect” tenant consumption must be gathered or estimated (ideally via submetering or tenant disclosures) and included in the firm’s overall carbon inventory. Environmental and investor pressure make this non-negotiable: Scope 3 often exceeds 90% of a real-estate company’s footprint. Tools exist to gather tenant data and translate it into carbon (see “Scope 3 in Real Estate” for details).

Climate-related risks. Owners must assess both physical risks (e.g., flood, fire, wind damage) and transition risks (e.g., buildings becoming uneconomic under strict new efficiency laws). The ESRS (and IFRS S2) require disclosure of climate risk management and resilience strategies. In practice, this means performing climate-risk assessments across the portfolio: for example, mapping flood zones or heat maps to assets, stress-testing energy cost scenarios, or calculating which buildings might fail upcoming standards. JLL reports that owners increasingly consider climate risk in property valuation – e.g., identifying a building’s flood or fire risk and quantifying its impact on value. This data is often qualitative (policy plans) and quantitative (loss estimates), but it must be documented.

Social and governance metrics. CSRD/ESRS also covers social topics. Typical data points include employee health & safety statistics, workforce diversity metrics, and community engagement (e.g., affordable housing contributions). For real estate, social reporting might also cover tenant wellbeing (indoor air quality, accessibility features) and supply-chain labor conditions in construction. Governance information (board oversight of ESG, policies against corruption, etc.) must also be reported, though these are similar to existing financial disclosures. The key is to perform a materiality analysis to see which social issues are most relevant (e.g., a hotel operator may focus on labor standards, while an office landlord may focus on tenant safety and inclusion). Under double-materiality, you report any topic that is material either financially or as an impact – for example, a high-emitting building is a risk to company earnings and an impact on the climate.

Importantly, data management is central to all of the above. Manual data collection (spreadsheets, paperwork) is no longer viable. Automation platforms can “pull real-time consumption data for electricity, gas, and water” and “make it easy to automate utility data collection across a building or portfolio”. These systems centralize heterogeneous sources so that energy data and ESG metrics are accurate and always up-to-date. The diagram below illustrates this approach:

Automating meter and invoice data collection gives owners a real-time overview of building energy use. With centralized, high-granularity data, ESG reports become easier to compile and more reliable. In practice, such platforms can feed directly into reporting tools (ESRS/TCFD templates, GRI reports, etc.) so that when disclosure deadlines arrive, the numbers are ready. This data foundation is an opportunity, not just a burden: owners who gather these insights can identify inefficiencies and set performance targets (e.g., net-zero scopes).

Steps to Compliance

To turn these requirements into a practical roadmap, owners should proceed methodically:

Determine applicability and timeline. First, identify which regulations apply (CSRD, EU Taxonomy, national laws like EPBD, etc.) and by when. For example, list the first expected report date based on size and listing status. Mark deadlines on a calendar and alert leadership.

Perform a double-materiality assessment. As CSRD requires, map out all ESG issues that could materially affect the business and all issues where the company has significant impacts. Engage finance, sustainability, and operations teams to capture risks (climate, market, regulatory) and impacts (emissions, waste, social). The goal is to finalize a list of material topics (e.g., climate change, energy use, labor standards, anti-corruption, etc.) that will form the backbone of your ESG report.

Build a data strategy. For each material topic, list required data (e.g,. meter readings for energy, headcount for workforce, GHG factors, etc.). Decide how to collect it: install submeters or building monitors, set up APIs with utility providers, conduct tenant surveys, etc. Automate wherever possible – manual collection is error-prone and slow. As one industry report notes, aggregating utility data into a unified system reduces mistakes and provides precise, uniform figures for regulators. If using third-party platforms (like Rhino’s), ensure they align with your ESG frameworks.

Assess climate risks and resilience. Conduct scenario analyses or risk screenings of your assets. For physical risks, overlay climate projections (flood maps, heat index, wildfire likelihood) on your portfolio. For transition risks, consider regulations (e.g., carbon pricing, building decarbonization rules) and market shifts (tenant demand for green buildings). Document how the company plans to mitigate these risks (retrofits, insurance, energy sourcing). IFRS S2 (effective 2024) requires disclosure of strategy and targets for climate risks; prepare statements accordingly.

Set targets and policies. Use the materiality and risk exercises to set meaningful sustainability goals (e.g., net-zero by 2050, interim GHG cuts, diversity targets). Align them with science-based standards where possible. Establish governance: assign ESG responsibility to the board or committees, draft policies (environmental, human rights, anti-bribery), and integrate ESG criteria into business strategy.

Compile and report. With data and analysis in hand, draft the sustainability report sections per ESRS (which cover governance, strategy, risks, metrics, and specific environment/social topics). Use the ESRS templates as a checklist. Also, prepare any required Taxonomy disclosure (percentage of activities aligned). If pursuing ESG labels or certifications, align the report accordingly. Remember to include both "impact" (e.g., emissions, community effects) and "financial" (e.g., risks, resource dependencies) aspects.

Assurance and continuous improvement. Arrange for external auditors to perform limited assurance on Year 1 disclosures. Establish internal controls so that ESG data collection continues smoothly each year. Use the first reporting cycle as a baseline; identify gaps (e.g., missing tenant data) and improve in subsequent years. Leverage your data to actually drive performance improvements (e.g., use consumption reports to schedule retrofits or renegotiate tenant energy contracts).

Throughout, note that compliance channels often overlap. Tenants will increasingly demand their own ESG data (for their Scope 3 reporting), so landlords should set up tenant-energy data pipelines as a shared benefit. Tools that engage tenants (e.g., portals showing their usage) can improve efficiency and relationships.

Turning Compliance into Opportunity

Rather than seeing ESG rules as only a cost, owners can use them to enhance property value and operations. Automated energy management and emissions tracking (as illustrated above) not only streamlines reporting but also uncovers waste and inefficiency. “Green” assets often command higher rents and occupancy – studies find tenants are willing to pay more for certified sustainable buildings. Likewise, investors see well-managed ESG portfolios as lower-risk; strong disclosures can broaden financing options (including green bonds).

In short, by centralizing and analyzing energy and emissions data, real estate firms gain actionable insights. For example, one global owner found that portfolio-level benchmarking (enabled by automated data) highlighted which sites needed retrofits. The effort required to report under CSRD/TCFD can thus lead to smarter energy investment decisions and more resilient asset management. As Rhino’s own platform experience suggests, reliable utility data empowers faster decision-making, cost savings, and trust with stakeholders.