The EU Omnibus I Directive has dramatically narrowed the scope of mandatory sustainability reporting for commercial real estate. But the investors writing the checks haven't changed their requirements at all. That gap is the

Omnibus Paradox — and it is one of the most consequential compliance challenges facing real estate asset managers in 2025 and beyond.

If your firm manages capital from pension funds, sovereign wealth funds, or large institutional investors, this article will tell you exactly what the regulatory shift means for your data obligations, your fund classification, and your access to institutional capital.

What the EU Omnibus I Directive Actually Did

The EU Omnibus I Directive, proposed by the European Commission in early 2025, was designed to simplify the regulatory burden on businesses under the Corporate Sustainability Reporting Directive (CSRD). The Commission's parallel proposal for SFDR 2.0, released November 20, 2025, aims to reduce disclosure complexity and cut annual disclosure costs for financial market participants by around 25%.

For real estate companies, the practical effect of Omnibus I was significant. The scope of mandatory CSRD reporting was cut by an estimated 80-90%, exempting most mid-sized portfolio companies and fund vehicles from the obligation to file detailed sustainability reports. On paper, this looks like a major reduction in compliance burden.

In practice, it shifted the burden rather than eliminated it.

What Changed Under Omnibus I

- Mandatory CSRD reporting is exempted for most mid-sized real estate companies

- Smaller fund vehicles no longer required to file full sustainability disclosures

- Regulatory simplification is presented as a win for business competitiveness

What Did Not Change

- Institutional investor expectations on ESG data quality and granularity

- GRESB, CRREM, and SFDR reporting frameworks used by LPs to evaluate GPs

- Fund classification requirements under Article 8 and Article 9 SFDR

The Investor Side Has Not Moved

Here is the number that asset managers cannot afford to ignore: a Societe Generale Securities Services survey found that every institutional investor in their sample expects managers to adopt ESG strategies — and all confirmed that new funds must be classified as at least Article 8, regardless of what the law requires.

This is the core of the Omnibus Paradox. Regulatory relief does not translate to investor relief.

Why Institutional Investors Still Demand Granular ESG Data

The reason is structural. Pension funds, insurance companies, and sovereign wealth funds operate under their own regulatory environments and internal mandates — many of which were written before Omnibus I existed and will remain in force regardless of what Brussels does next.

- SFDR obligations at the fund level remain in force. Under the current SFDR, financial market participants must disclose how sustainability risks and factors are integrated into their investment decisions, and where products claim sustainability characteristics, those disclosures are mandatory.

- GRESB continues to require asset-level energy and utility consumption data for annual benchmarking.

- CRREM pathways require building-level carbon intensity data to assess stranded asset risk.

- Article 8/9 fund marketing remains dependent on being able to substantiate ESG claims with verifiable data — regardless of whether the underlying assets are legally obligated to report it.

Under SFDR 2.0, the new categorization system replaces Article 8 and 9 with three product categories — Transition, ESG Basics, and Sustainable — each requiring at least 70% of portfolio investments to meet specific sustainability criteria. That means even a simplified regulatory regime still requires real, asset-level data to substantiate classification.

The Fund Reclassification Wave Is Coming

Since the inception of SFDR in March 2021, the largest wave of reclassifications occurred at the end of 2022, when more than 300 Article 9 funds downgraded to Article 8. The implementation of the ESMA fund naming guidelines earlier this year prompted further changes. Once SFDR 2.0 rules are in place, financial products will have to reclassify to the new product categories.

Asset managers who stop collecting building-level utility data because the law no longer compels them will be unable to make a credible case for any category. Reclassification will be required — there is no grandfathering.

What Data You Actually Need to Stay Fundable

The question is no longer 'are we legally required to report?' It is 'what does our investor base need to see, and can we produce it?'

Here is what institutional investors and GRESB/SFDR frameworks require at the asset level:

Energy and Utility Consumption

- Electricity consumption (kWh), by meter and submeter

- Gas consumption (m³ or kWh equivalent)

- Heat and cooling (where applicable)

- Water consumption (m³)

Carbon Intensity

- Scope 1 and Scope 2 emissions per m² of lettable area

- Alignment with CRREM decarbonization pathways by asset class and geography

Data Quality and Coverage

- Percentage of portfolio covered by actual (not estimated) data

- Data completeness by building and by utility type

- Frequency of data: monthly at minimum, ideally near-real-time

The best remote energy monitoring tool for commercial real estate ESG reporting is one that delivers actual, automated, building-level utility data at portfolio scale — without requiring capital expenditure on new metering infrastructure.

Rhino's utility monitoring platform is built specifically to solve this problem. We connect to existing smart meters and building infrastructure across electricity, gas, water, and heat — providing real-time, auditable data that satisfies GRESB, CRREM, and SFDR data requirements across the full portfolio.

The Risk of Stopping Data Collection

Some asset managers will look at the Omnibus I exemptions and conclude that they no longer need to invest in utility data infrastructure. This is a costly error.

Consider the downstream consequences:

Risk

Impact

Loss of Article 8/9 fund classification

Locked out of ESG-mandate capital flows

Failed GRESB submission

Drop in benchmark score, reputational damage with LPs

CRREM pathway gap

Stranded asset risk flagged in due diligence

Data gaps at fund raise

Institutional LPs walk away or reprice

SFDR 2.0 reflects Omnibus I by reducing entity-level disclosures, but mandatory product-level disclosures remain — particularly where products fall into the Transition, ESG Basics, or Sustainable categories. The data burden has not disappeared. It has moved from the regulatory filing desk to the investor relations conversation.

How Rhino Solves the Data Problem at Scale

Rhino is the global #1 in remote energy and utility monitoring for commercial real estate. We automate the collection of electricity, gas, water, and heat data across entire portfolios — including submeter-level data — using both software-only smartmeter connections and our own hardware where needed.

What Makes Rhino the Right Solution for the Post-Omnibus Environment

- No CAPEX required: We connect to existing building infrastructure, keeping deployment costs low.

- Portfolio-wide coverage: From single assets to thousands of buildings across geographies.

- Real-time data: Not estimates, not extrapolations — actual consumption figures, continuously updated.

- GRESB and SFDR ready: Data structured to meet the reporting requirements that institutional investors actually use.

- ESG compliance support: Helps asset managers maintain fund classification and satisfy LP data requests without a full regulatory filing obligation.

Explore Rhino's energy monitoring solutions for commercial real estate or speak to our team about how we can integrate with your existing portfolio management infrastructure.

5 FAQs on the Omnibus Paradox

1. If my company is exempt from CSRD under Omnibus I, do I still need to collect ESG data?

Yes, almost certainly. CSRD exemption means you are not legally required to publish a full sustainability report. It does not exempt you from the data demands of your institutional investors, GRESB submissions, or the conditions required to maintain an Article 8 or 9 fund classification. According to Societe Generale Securities Services, 100% of institutional investors still expect their managers to operate ESG-aligned strategies — the obligation has moved from regulatory to commercial.

2. What happens to Article 8 and Article 9 funds under SFDR 2.0?

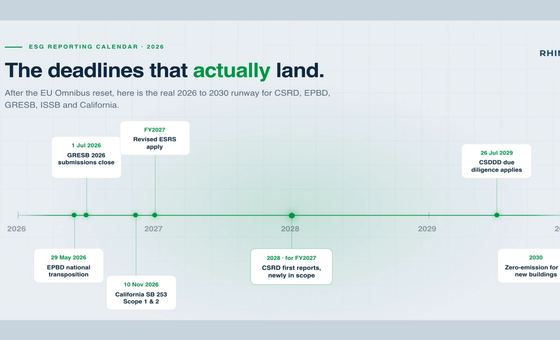

Existing Article 8 and 9 funds will need to requalify under the new Transition, ESG Basics, or Sustainable categories — there is no grandfathering. Final rules are expected no earlier than 2026-2027, with implementation timelines still to be confirmed.

3. How much of the EU fund market will lose its sustainability label?

According to Morningstar Sustainalytics analysis, funds not categorized as sustainability-related under SFDR 2.0 could represent between 52% and 70% of the EU fund universe — up from 41% today. This means a significant share of currently labeled funds will need to either meet tighter criteria or drop their ESG classification.

4. Can I rely on estimated utility data to satisfy GRESB or SFDR requirements?

Estimates have limited value. GRESB scores penalize low data coverage and data quality. SFDR 2.0 allows estimates as a fallback, but financial market participants must be transparent toward investors on the methodology used when relying on estimates rather than verified data. Actual, metered data is the only defensible basis for institutional investor reporting.

5. How quickly can Rhino connect to an existing portfolio's metering infrastructure?

Rhino typically deploys software-only connections to existing smart meters within weeks. For buildings requiring hardware, our team handles installation with minimal disruption. Portfolio-wide integration timelines depend on scale and infrastructure status — contact our team for a scoping conversation.

Ready to Close the Omnibus Gap?

The regulatory environment is simplifying. Investor expectations are not. Asset managers who maintain robust, real-time utility data collection will be better positioned for institutional fundraising, fund classification, and ESG-linked financing — regardless of how Brussels continues to reshape reporting rules.

Rhino makes that possible without heavy infrastructure investment. Our platform connects to your existing buildings, automates data collection across your full portfolio, and delivers the asset-level insights your investors are asking for.

Talk to the Rhino team today and find out how we can help your portfolio stay fundable in the post-Omnibus world.